Abstract

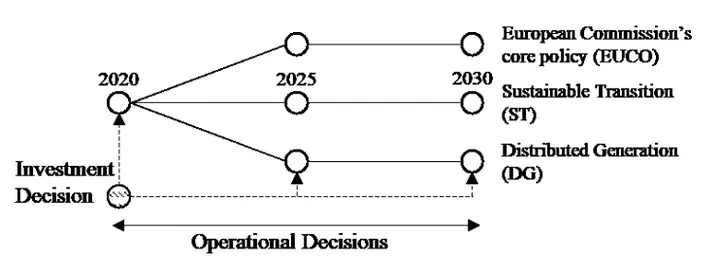

As energy markets underlie significant uncertainties, predictions regarding future developments are difficult and ex-post often proven wrong. In this paper, we develop a two-stage stochastic cost-minimization model of integrated European electricity and gas markets. The model identifies optimal investment decisions in power generation capacity and the scenario-specific optimal dispatch for assets in electricity and gas sectors. The paper presents a regret matrix that examines the performance of first-stage investment decisions under the later realization of considered scenarios. We find that the chance of high regrets strongly depends on the scenario the investment decision is based on. Furthermore, we analyze the impact of each uncertain parameter on the expected regret. We find that neglecting uncertainties with regard to electricity demand levels and CO2 prices in particular, result in a high regret. Furthermore, we quantify the value of perfect information.